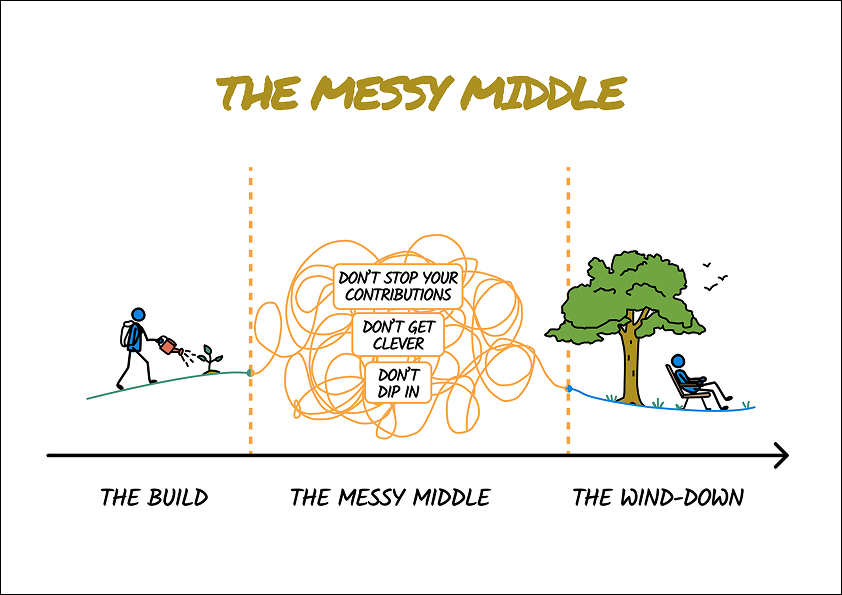

Working life tends to be split into three phases. There’s the early stretch, when you’re setting things up and putting your financial structure in place. There’s the final stretch, when you’re winding down towards retirement. Between these two phases, there’s the long middle stretch where most of life actually happens.

In this middle phase, the main work of building your financial structure is done. The accounts are open, and the contributions are running in the background. The investment strategy was chosen years ago and likely doesn’t need to be reinvented. From here on, your job isn’t to add something clever; it’s to leave the structure alone and let it do what it was designed to do.

Unfortunately, the temptation to interfere with a plan is strongest precisely during the stretch of life when such interference is most damaging.

The Busy, Messy Middle

The middle stretch of working life is demanding for many reasons. Careers are at full intensity. Kids are at their costliest, whether that’s school fees, university, or the years just before they leave home. Parents are starting to need help in ways they didn’t before. Mortgages are real. Cars need replacing. A holiday that used to be frugal is now a major expense.

It’s also the stretch where you have the least bandwidth to think about the future. Decisions about money get squeezed into the gaps between everything else, often made quickly and under pressure.

Because of the demands on your time, energy, and money, this phase of life is exactly when the structure you built is most at risk.

The Three Ways People Interrupt the Machine

We’ve seen families damage their financial lives in a variety of ways. But three specific actions show up time and again.

The first is to reduce or pause contributions. Life happens, and something has to give. The plan is always to catch up later, when things settle. In practice, we see that the contribution paused for a year often remains paused, and the compounding effect of that decision is lost forever.

The second is getting too clever. Well-meaning friends describe a complicated structure that saves tax or an alternative investment that’s been performing well. In the moment, the tried-and-tested approach seems outdated, and the novel approach appears enticing. The temptation to optimise feels productive, especially when life elsewhere feels out of control. But the strategy you chose years ago was chosen for a reason, and tinkering with it now often adds cost and complexity without improving the outcome.

The third mistake is dipping into long-term investments for lifestyle expenses. It could be a renovation, a bigger car, or something that gives your child a head start over their peers. Each decision is defensible, but the consequences for your long-term financial independence become a problem for your future self.

The Discipline of Restraint

Because the pressure to interfere is constant and the justifications are usually reasonable, restraint during this phase of life requires real discipline.

Consistent contributions and uninterrupted time during this “messy middle” are a major driver of financial independence later in life.

Perfect discipline is not always achievable, but this is what we encourage clients to aim for:

- When money is tight, make your contributions the last thing you reduce, not the first.

- When a new idea or structure comes up, ask whether it’s actually better than what you have, or just newer and more interesting.

- When something tempting comes up that would require dipping in, ask whether the cost is worth what it might mean for your long-term plan.

If you’re in the busy, messy middle and you already have a financial plan in place, the most useful thing you can do is to get out of your own way. If something has come up that’s making you consider changing course, talk to us before you do. In most cases, the plan you committed to years ago is still the right one to stick with.

Risk warnings

This article is distributed for educational purposes only and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy, or investment product. Reference to specific products is made only to help make educational points and does not constitute any form or recommendation or advice. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.