Inflation: Transitory No More?

January Woes

January is my least favourite month; indeed, the most depressing day of the year “Blue Monday” falls in January. But for me, it’s not the grey skies, the cold, or the realisation that Christmas pudding cannot be legitimately eaten for breakfast for an entire year that makes me so glum. You see my low mood is caused by the cost of running Bertie, don’t we all have a name for our cars? Being so organised, my other half would argue, disorganised, I have managed to synchronise all the major expenses of running Bertie to fall in January – it’s an expensive month!

Of all the expenses, insurance is the one I dread. You see, Bertie was purchased more with heart than head, yes, I admit it, he was a mid-life (early I hasten to add), crisis purchase. I will say no more! So, I’m well prepared to fall off my chair when I open the renewal quote and have become rather adept at justifying the expense. Indeed, chair falling did occur this year but for a very different reason. To my shock, my renewal quote had dropped almost by half. I’d like to believe that the insurance company finally trusts me to drive sensibly but unfortunately, I think it’s more to do with hitting a certain age, the pandemic, and changes to regulations. Whatever the reason, it’s very much welcomed, as every other bill seems to be rising at the moment.

Good in Moderation?

If only all bills were falling by 50%! You would think that would be a good thing? Well, deflation can contribute to lower economic growth, this is a problem for investors as equity market returns are strongly linked to the long-term performance of the economy. Deflation increases the real value of money and debt. This makes it more difficult to repay debt, and consequently, consumers and businesses have less to spend and invest. Deflation also encourages people to hold off on spending, particularly on luxury and non-essential items, anticipating that prices will drop in the future, again, reducing economic growth.

So, as strange as it seems, some inflation is a good thing and can be a sign of a healthy economy. When consumers expect prices to rise this encourages them to spend now, which in turn provides businesses with the money needed to grow. Japan’s “Lost Decade” was a ten-year period between 1991 and 2001 that saw the once-bustling Asian economy stagnate, in part, due to the impact of deflation. While most central banks worry about curbing inflation, the Bank of Japan has been trying to increase inflation for almost a decade to meet its target of a long run 2% rate, without much success.

Prices Are Up

If inflation increases as expected this is not a problem, as consumers, businesses and investors have built these expectations into their wage negotiations, product prices, and investment returns. It’s when inflation increases to unanticipated levels that central banks get the jitters. Let’s take Edward for example, he has shrewdly negotiated a pay deal so his salary will increase in line with expected inflation over the next 3 years, this means his buying power will remain the same. If, however, inflation increases more quickly, his purchasing power is reduced, and he is poorer in real terms. In response, he will demand higher wages, which can trigger further inflation as his firm increases prices to fund the salary increase.

Unfortunately, prices are rising, and at rates not seen for many years. In the UK, inflation is running at a 10 year high, at 5.1% as measured by the Consumer Price Index (CPI) and 7.1% using the Retail Price Index (RPI)(Office for National Statistics (2022)). Although the RPI is no longer an official national statistic; the method of calculation is believed to overestimate inflation, it remains important for consumers as it is still used to index price increases for several items such as train tickets, car tax and interest on student loans. Prices are not just rising fast in the UK. Inflation has risen to 4.9% (European Commission (2022)) in the Eurozone, the highest level since the Euro was introduced in 1999, while in the USA, inflation is at a 40 year high, at 6.8% (US Bureau of Labor Statistics (2022)).

Source: ONS (2022)

Current Drivers of Inflation

The inflationary pressures that started to build during 2021 were not totally unexpected. Strict lockdowns in 2020 shutdown the world economy. While the production of many goods and services ceased, many consumers started to accumulate savings; either their incomes were protected by government schemes, or they were able to continue to work remotely and had little opportunity to spend.

When economies started to re-open, consumers were immediately ready to open their purses and wallets. Unfortunately, it takes time for production facilities and supply chains to reach full capacity once they have been closed. With a mismatch between strong demand and weak supply, bottlenecks and backlogs were to be expected, these ultimately resulted in price increases.

In March, a very real-world example of how bottlenecks can impact the world economy occurred when a container ship ran aground in the Suez Canal and blocked it for six days. Ordinarily, container ships are rarely discussed, they are the unsung heroes of global trade but when the Ever Given got stuck the whole world took notice. Why? Because the Suez Canal is one of the busiest trade routes in the world, each day 12% of global total trade moves through this narrow waterway. With the canal blocked, an estimated $9.6bn dollars of trade per day was held up (Bloomberg (2021)). The blockage resulted in further pressure being applied to an already strained supply chain and underscored the fragility of global trading networks.

Labour market pressures were a further contributory factor to rising inflation. There was a substantial increase in those people of working age taking early retirement, an increase in people leaving their jobs seeking a better employment “match”, absenteeism, and manpower constraints. This put further pressure on the ability of economies to quickly restart and reach full levels of production (D’Acunto & Weber (2022)).

The UK provided a prime example of how labour market pressures can impact inflation. In September, rumours of fuel shortages resulted in panic buying, fuel prices increased to their highest levels for eight years and eventually petrol stations ran dry (The Times (2021)). There was no shortage of fuel, rather a shortage of heavy goods vehicle (HGV) drivers. We saw a combination of Brexit, which had made it more difficult for European nationals to work in the UK, together with an increase in the number of people leaving the industry during the pandemic and a reduction of new drivers being trained as lockdowns had closed driving centres; all coming together to bring the country to a standstill.

Central Banks are Stirring

Since the pandemic began, policymakers have strived to protect their economies from the impact of lockdowns. Central banks cut interest rates to record lows while governments announced various stimuli and support packages, all designed to prevent long term damage to their respective economies. As 2021 began, inflationary pressures started to rise but economic growth was deemed to be more important than the threat posed by inflation. It was only as the year came to an end, that central banks looked ready to address the inflationary pressures.

The standard policy response to increasing inflation is to increase interest rates. As money becomes more expensive to borrow, this encourages people to save more and spend less, lowering the demand for goods and services, reducing price increases.

In December, the Bank of England broke ranks and became the first central bank of a major economy to announce an increase in interest rates since the start of the pandemic; up 0.15% to 0.25%, from a historic low of 0.1%. The decision followed a surprisingly sharp increase in inflation to 5.1% during November, up from 4.2% in the previous month, well ahead of the Bank’s forecast that inflation would “comfortably exceed 5% when the Ofgem cap on retail energy prices is next adjusted, in April” (Bank of England (2021)). Further pressure to act was applied by the International Monetary Fund in its annual report on the British economy, which warned the Bank of England not to act too slowly to avoid “inaction bias” (International Monetary Fund (2021)). Markets reacted somewhat with surprise to the increase, given the recent emergence of the Omicron variant and its potential impact on the economic recovery.

In the US, policymakers also appear to have revaluated their position on inflation. At the end of November, Jerome Powell, the Chair of the Federal Reserve told the Senate Banking Committee that it was probably time to retire the word “transitory” when describing inflation, noting that “inflation has been more persistent and higher than we’ve expected” (US House Committee on Financial Services (2021)). In mid-December the Federal Reserve announced its intention to scale back the financial stimulus that had been introduced in the wake of the pandemic more quickly than originally planned, together with expectations that three interest rate increases were likely in 2022, the first potentially as soon as March (Federal Reserve (2021)).

And it’s not only in developed markets where central banks are increasing interest rates in an effort to tame inflation. In December, rate rises were announced in Armenia, Chile, Costa Rica, Hungary, Mexico, Pakistan, and Russia. As with their more developed counterparts, many of these countries’ central banks indicated further interest rate rises will come next year.

Even in Japan, where deflation rather than inflation has historically been an issue, the Bank of Japan has dialled back some of its pandemic monetary support (The Japan Times (2021)).

Inflation’s Friend… Poor Policy

The prospect of future interest rate rises and their potential impact on economic growth and ultimately stock market returns will undoubtedly cause some investors anxiety. However, investors should be more concerned when central banks fail to step in and moderate inflation with prudent and responsible interventions. Turkey is a case in point, annual inflation rose to 36.1% in December, up from 21.3% the previous, month (Central Bank of the Republic of Turkey (2022)). The key driver of inflation has been a fall in the value of the lira. At the start of the year, $1 was worth ₺7, by year-end, $1 would buy almost ₺13. Turkey is heavily reliant on imported energy and goods, as the lira has fallen in value, higher costs have been passed on to the consumer.

Turkey’s problems can be attributed to President Erdogan’s “economic war of independence”, policies designed to revitalise the Turkish economy. Contrary to economic principles that raising the cost of borrowing helps to curb high inflation, the President believes that “interest rates are the mother of all evils” (Financial Times (2018)) and has been sacking any governor of the supposedly independent Central Bank of the Republic of Turkey that disagrees with him; three in total since 2019. This helps to explain why despite rising inflation the central bank has continued to lower interest rates.

Given the economic and political history of Turkey, President Erdogan’s approach to inflation is all the more perplexing. Turkey’s inflation rate is at its highest level since September 2002, when it reached 37%, which together with the continuing fallout of the Turkish Economic Crisis of 2001 helped pave the way for his very own Justice and Development Party (AKP) to win a landslide victory in November 2002 (Reuters (2022)). Without a swift revaluation of economic policy, the President may well end up being swept from power, ironically for the same reasons his party originally took power nearly two decades ago.

Value in Inflation?

Investors undoubtedly have good reason to be wary of inflation. However, value investors can benefit from rising prices. Value investing is a strategy whereby investors seek to identify stocks that are currently undervalued by the market. The intention is to buy these “cheap”, value stocks and profit from their eventual increase in price. The opposite strategy is that of growth investing, whereby investors attempt to identify firms whose revenue and earnings will grow faster than the market average.

Value and growth stocks frequently traded position during 2021 as the best performing investment strategy. By the end of the year, however, value stocks had won out, returning 20.7% compared to growth stocks, which returned 18.2% (Global Growth Stocks: MSCI ACWI Value; Global Value Stocks: MSCI ACWI Value. Performance period: 31/12/2020 – 30/12/2021).

Source: FE Analytics (2022) (Global Value Stocks: MSCI ACWI Value; Global Growth Stocks: MSCI ACWI Value)

Over the long term, growth stocks continue to deliver greater returns and the pandemic has only exacerbated this trend. Lockdowns disproportionately affected value stocks, which tend to be more cyclical, for example, energy, retail, and transport. Growth stocks were more resilient and some, for example, technology stocks, even benefited from the restrictions.

However, value companies with real assets, debts that will be eroded by inflation and the ability to raise prices, are more favourably positioned to take advantage as inflation rises. Research from Fama and French shows that during decades of high inflation, the 1940s, 1970s and 1980s, value stocks outperformed. During the 1930s, 1990s and 2010s, when inflation was low, growth stocks outperformed (Wall Street Journal (2021)).

Whether value stocks are poised for a sustained resurgence driven by inflationary pressures depends on how persistent price rises become. If the “transitory” inflation of 2021 becomes more “permanent” in 2022 and beyond, value investors should be well-positioned to take advantage.

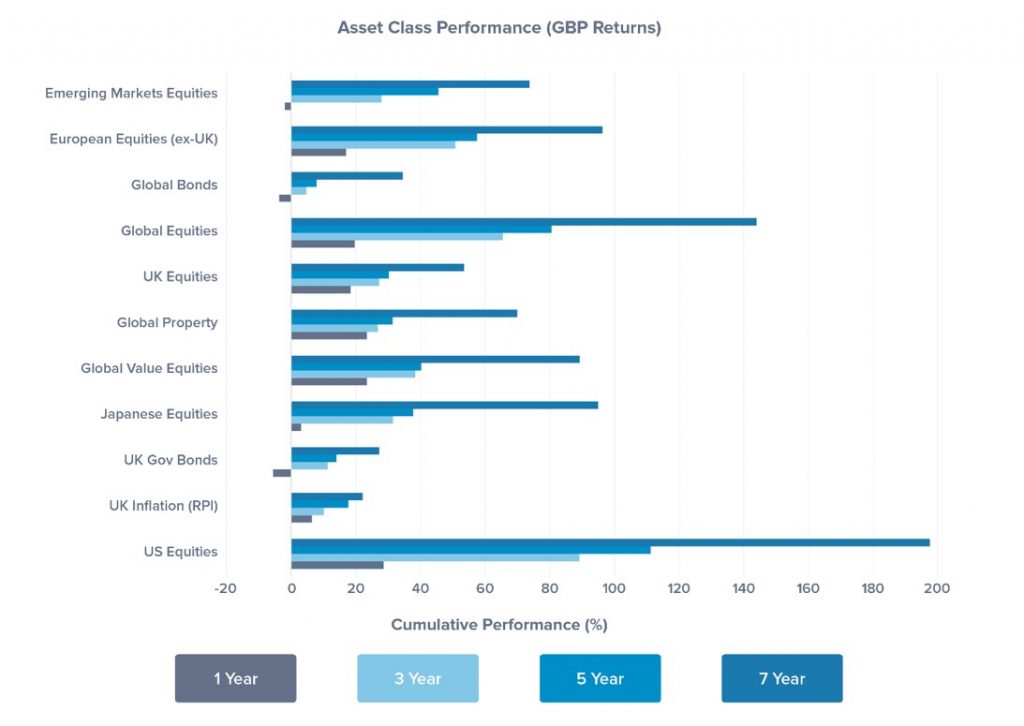

Asset Class Returns

Somewhat Déjà Vu

Since the initial shock of the pandemic caused equity markets to drop in early 2020, each subsequent quarter has felt very similar to the last. The fourth quarter of 2021 was no different.

Developed market equities continued to rally despite the emergence of the Omicron variant, which caused a spike in market volatility as the year drew to a close. This volatility was short-lived, however, as data indicated that although more infectious, the new variant was less severe than originally feared.

Source: FE Analytics (2021) (Global Bonds: Bloomberg Global Aggregate, UK Government Bonds: Bloomberg Global Aggregate UK Government Float Adjusted, UK Equities: FTSE All Share, Global Property: FTSE EPRA Nareit Global, Emerging Markets Equity: MSCI Emerging Markets, EU Equities (ex-UK): MSCI Europe ex UK, Japanese Equities: MSCI Japan, US Equities: MSCI USA, Global Value Equities: MSCI World Small Value, Global Equities: FTSE Global All Cap, UK Inflation (RPI): UK Retail Price Index. Performance periods: 1 Year: 31/12/2020 – 31/12/2021; 3 Year: 31/12/2018 – 31/12/2021; 5 Year: 31/12/2016 – 31/12/2021; 7 Year: 31/12/2014 – 31/12/2021).

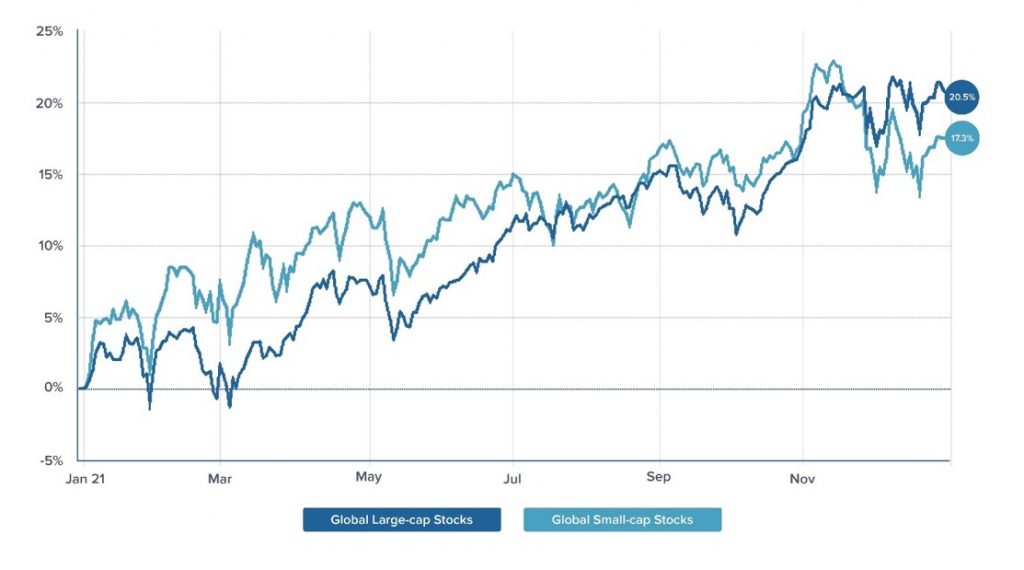

Small-caps had returned 15.3% compared to 12.6% for large-caps over the first three quarters of 2021 (Small-cap: MSCI ACWI Small Cap; Large-cap: MSCI ACWI Large Cap. Performance period: 31/12/2020 – 30/09/2021). Small-cap companies’ fortunes are closely linked to the overall economy and as such were disproportionately affected during the events of early to mid-2020. However, in the final quarter of 2020, as signs that economic recovery could be fast approaching, smaller firms, whose stocks were cheaper once again becoming an attractive proposition. This momentum continued well into 2021 but slowed as uncertainties over the sustainability of the economic recovery increased. By year-end, small-cap stocks had underperformed their large-cap counterparts by 3.2%.

Source: FE Analytics (2022) (Global Large-cap Stocks: MSCI ACWI Large Cap; Global Small-cap Stock: MSCI ACWI Small Cap. Performance period: 31/12/2020 – 31/12/2021).

Interestingly, as this year began, the International Monetary Fund (IMF) announced that the January update to its bi-annual report, The World Economic Outlook, will be delayed “to allow our teams to incorporate the latest developments related to the COVID-19 pandemic into the economic forecasts” (The Economic Times (2022)). This may suggest a downgrade to economic growth forecasts in 2022 are coming.

Concerns regarding inflation and Omicron and their impact on the world economy caused The Centre for Economics and Business Research (CEBR) to revise its global economic growth forecast down to 4% for 2022 at the beginning of January; down from an estimate of 5.1% made in 2021 (Centre for Economics and Business Research (2022)).

The future as always is uncertain, and the potential impact of rising inflation and Omicron on the global economy will inevitability cause many to forget how strong the recovery was in 2021. The IMF estimated that global economic growth was 5.9% in 2021. Compared to 2020 when national lockdowns caused the world economy to grind to a halt, resulting in a -3.1% decline in economic growth, 2021 was a very good year (International Monetary Fund (2021)). As we noted in the last quarterly review, such high levels of economic growth have not been seen since 1973, when the global economy grew by 6.5% (World Bank (2021)).

In the US, numbers were even better, with economic growth estimated to be 6% in 2021 compared to -3.4% in 2020 (International Monetary Fund (2021)). Why is this so important? Because despite the unrelenting rise of China as an economic power, the US is still the engine that drives the world economy and the old adage of “when America sneezes, the world catches a cold” is still very much true.

Source: IMF (2021) (International Monetary Fund (2021). Please note, projections are as of October 2021).

The US economy was helped in 2021 by President Biden’s aggressive policies to tackle coronavirus together with trillion-dollar initiatives, such as the American Jobs Plan (AJP), designed to improve the countries creaking infrastructure and create thousands of jobs in the process. Unsurprisingly, markets reacted positively to such announcements. Despite increasing inflationary pressure and other uncertainties the S&P 500 returned 26.9% (S&P Dow Jones Indices (2022)) over the year.

In China, the year began with the economy firing on all cylinders, rebounding strongly from an underwhelming but still impressive economic growth figure of 2.3% during 2020. Considering an average growth figure of -4.5% for the Advanced Economies and -2.1% for the Emerging Market and Developing Economies, China’s performance during 2020 was all the more remarkable (International Monetary Fund (2021)).

By mid-year however, the Chinese economy began to cool rapidly. Despite the slowdown, the World Bank had projected economic growth in China of 8% by year end (The World Bank (2021)). A staggering figure indeed but both the IMF and World Bank have noted the momentum is slowing and forecast economic growth of 5.6% and 5.1% respectively in 2022. A substantial drop but compared to the average economic growth rates forecasted for Advanced Economies in 2022 such as Australia (4.1%), France (3.9%), Germany (4.6%) and Japan (3.2%), still impressive (International Monetary Fund (2021)).

In Europe, the third major economic force in the world, 2021 economic growth has also been robust, at 5% (International Monetary Fund (2021)). While an encouraging figure, the growth rates between countries within Europe vary widely. With the threat of new restrictions in response to Omicron and soaring energy prices exacerbated by political tensions with Russia, the continent’s biggest energy supplier, 2022 is likely to be a challenging year for European economies.

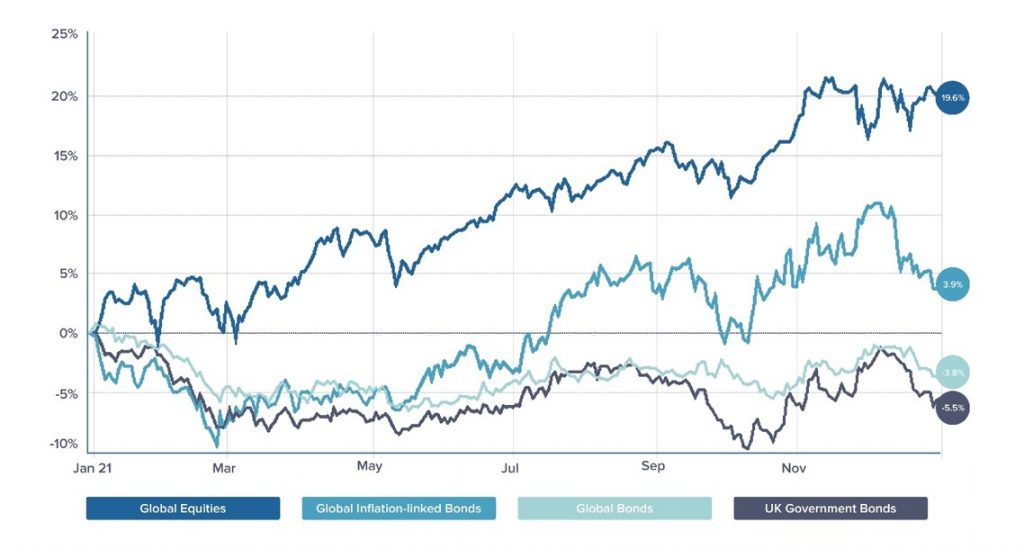

Source: FE Analytics (2022) (Global Equities: FTSE Global All Cap; Global Inflation-linked Bonds: Bloomberg Global Inflation-linked; Global Bonds: Bloomberg Global Aggregate; UK Government Bonds: Bloomberg Global Aggregate UK Government. Performance period: 31/12/2020 – 31/12/2021).

Bond markets have struggled during 2021, lagging equities, and the fourth quarter was no different. Compared to the third quarter, UK government bonds showed an improvement in performance, up from -2% to 2.8% while global bonds lost ground, falling from 1.4% to -1.1%. A review of the performance of global bonds and UK government bonds over the year shows both providing negative returns.

Compared to the returns of equity over the last year, investors can understandably question the rationale for continuing to hold such assets. Bonds provide a cushion when equity markets fall, softening the blow, decreasing the volatility of portfolio returns. When the pandemic hit in early 2020, the merits of holding bonds were all too apparent. When equity markets crashed, investors sought out less risky assets and bond prices rose.

What went wrong with bonds last year? In response to the pandemic central banks and governments the world over enacted policies in an attempt to protect their economies, typically via a combination of lowering interest rates and stimulus packages. These policies put pressure on bond yields, which increasing inflationary pressures over the year only exacerbated.

It was not all bad news for bond investors. Unsurprisingly, as inflation increased throughout 2021, global inflation-linked bonds also increased in value, up 3.9% (Global inflation-linked bonds: Bloomberg Global Inflation-linked. Performance period: 31/12/2020 – 31/12/2021) over the year. This highlights the importance of maintaining a diversified portfolio. Not only in terms of the different asset classes of bonds and equity but also within each asset class. Holding a diversified pool of bond assets means that while some bonds may currently be struggling and underperform due to exposure to a particular risk factor, other bond assets held could potentially be well placed to take advantage of that same risk factor.

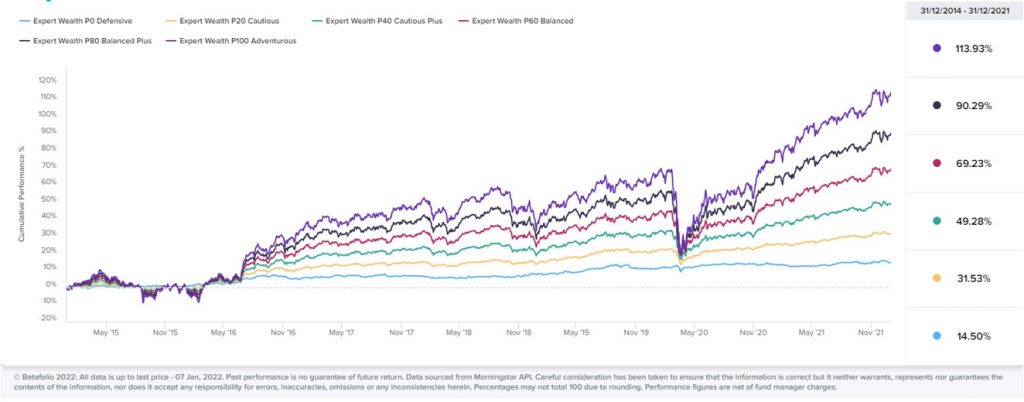

Portfolio Performance

(All data is up to the last price – 31 December 2021. Past performance is no guarantee of future return. Data sourced from Morningstar API. Careful consideration has been taken to ensure that the information is correct but it neither warrants, represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Percentages may not total 100 due to rounding. Performance periods: 1 Year: 31/12/2020 – 31/12/2021; 3 Year: 31/12/2018 – 31/12/2021, 5 Year: 31/12/2016 – 31/12/2021, 7 Year: 31/12/2014 – 31/12/2021. Additional performance periods may be accessed with the help of your adviser via the Betafolio Control Centre: https://app.betafolio.co.uk.)

Looking at the 2021 returns for Expert Wealth and Expert Wealth ESG portfolios, the momentum gained from Q2 2020 continued into 2021, and it was positive through the first three quarters. But in the last quarter of 2021, the momentum has slowed down due to the Omicron variant’s rise and the increasing inflation rate. Still, all portfolio ranges across both portfolios have remained in positive territory. The 1 year, 3-year, 5-year and 7-year performances have all seen an overall growth. Overall, the equity heavy portfolios have outperformed as expected.

Expert Wealth Cumulative Gross Performance

Source: Betafolio (2022)

Source: Betafolio (2022)

Expert Wealth ESG Cumulative Gross Performance

Source: Betafolio (2022)

Source: Betafolio (2022)

Closing Remarks

As 2021 began, any remaining festive cheer was soon replaced by news of a second national lockdown in response to the Delta variant. Although disruptive, the restrictions did not impact the economy to the same extent as those introduced during 2020; this time around, people and businesses were better prepared.

Restrictions were lifted slowly over the following months, but it was mid-July before most legal limits on social contact were finally removed and the final sectors of the economy reopened. Even then, official guidance urged caution.

As the months passed, we collectively dared to hope that we were at last returning permanently to normality but then: Omicron. New restrictions were imposed, and now as 2022 begins, it very much feels like January 2021 all over again.

The pandemic has truly made me appreciate the despair Phil, Bill Murray’s character felt, stuck in a time loop in the film Groundhog Day. I suppose one saving grace has been that, unlike Phil, I have not been woken every morning by “I Got You Babe” by Sonny & Cher.

But like Phil, the pandemic has taught us one important skill, that of resilience. Despite every setback and new challenge, we have kept moving forward, adapting how we live and work so that a return to normal life can happen as quickly as possible.

Resilience was also a key consideration when building your portfolio. Investing is never plain sailing, the last two years have made that abundantly clear and although the thought of investing while avoiding risk may seem appealing, investors are only rewarded for taking on risk. This is why your portfolio has been designed using decades of research so that it has the best possible chance of weathering any market headwind and providing the best possible returns over the long term.

Important Information

©2022 Expert Wealth Management. All rights reserved. Expert Wealth Management is a trading style of Expert Financial Solutions Ltd which is authorised and regulated by the Financial Conduct Authority. FCA No. 401295.

Past performance is no guarantee of future return. The value of investments and the income from them can go down as well as up. You may get back less than you invest. Transaction costs, taxes and inflation reduce investment returns.

The content of this bulletin is for education and information purposes only and should not be considered personal financial advice. Expert Wealth Management is not responsible for any action taken by clients as a result of this bulletin. Please contact us if you wish to discuss your portfolio.