In light of the US regulator’s (SEC) recent approval of several Bitcoin spot ETF’s, there has once again been a lot of talk around cryptocurrency and the exposure of client portfolios to this particularly volatile asset class.

Recent developments

On the 10th of January 2024 the Securities and Exchange Commission (SEC) approved the first ETFs that would directly hold, and track, the price of a bitcoin (For those eagle-eyed, grammar focussed readers the ‘b’ in bitcoin is not capitalised here. The official Bitcoin glossary states: ‘Bitcoin – with capitalization, is used when describing the concept of Bitcoin, or the entire network itself. e.g. “I was learning about the Bitcoin protocol today”. Bitcoin – without capitalization, is used to describe bitcoins as a unit of account. e.g. “I sent ten bitcoins today.”; it is also often abbreviated BTC or XBT.’), which is arguably the best known cryptocurrency. Prior to this, Bitcoin ETFs were listed on US markets, but these did not hold bitcoins directly, holding derivatives (futures) of the cryptocurrency, or investing in the shares of firms that were involved in the technology. The argument from those who wished to list direct holding ETFs was that the use of derivatives made the pricing mechanisms more complex and the products more expensive. Now that several of these direct holding products have been approved, providers hope that costs will come down, their value will go up and liquidity will increase due to an increase in daily trading through ETFs.

Has anything really changed?

The main question that arises around the news is does this approval change anything? In short, from our point of view, no. Firstly, the early signs are that price and volume have not surged on this news. In fact, at time of writing, the price of a bitcoin is down around 10% since the first direct ETF was launched. Secondly, and far more importantly, we do not believe it is an asset that should be held in portfolios.

It is simply a medium of exchange (like a normal currency), is a highly volatile store of value, is slow and expensive to transact, and lacks liquidity.

Furthermore, the industry has been marred by scandal after scandal. Most recently Binance, a cryptocurrency exchange, was fined $4.3 billion and CEO Changpeng Zhao was forced to resign over violations of money laundering laws. On the flip side, cryptocurrency and blockchain technology as a whole are a growing and highly innovative industry that may lead to future growth and return opportunities within traditional markets. As one may imagine, this can lead to a wide range of queries and concerns around investor exposure to the sector.

Why should you care about crypto?

While cryptocurrencies may not be something that an investor should include in a portfolio directly, it has become a sizeable area of the market. The current total value of cryptocurrencies sits at around $1.71 trillion. This figure does not, however, include the market cap of companies that have some exposure to the space, which could be as much as $16 trillion, depending on the definition used.

It is therefore not an industry that can be completely ignored, and it already indirectly makes up a portion of any well-diversified portfolio.

Calculating exposure of a fund or portfolio to crypto is a complex task as it is largely dependent on what constitutes a ’crypto stock‘. The definition ranges from companies that explicitly mine or hold bitcoins, or other cryptocurrencies, to companies that get some advertising or sponsorship money from digital assets. There are numerous examples of companies like this, that have a very small portion of their revenue linked to cryptocurrencies or blockchain technology but could be defined as having crypto exposure depending on the classification used.

In order to use a robust, but wide, definition of “crypto stocks” in this note, research from Morningstar was used to provide an estimate. The cited article uses a quantitative methodology to identify the stocks that are most correlated, both intentionally and unintentionally, to the cryptocurrency market. The list is shown in the figure below.

Source: Morningstar (The Morningstar research was published in March 2023 so the exact list may be slightly different if it were to be reproduced today)

Examining the list it is clear to see there are some stocks with direct links. Marathon Digital Holdings, Riot Platforms and Hut 8 Mining are crypto mining companies, their sole purpose is to generate new coins. There are also companies such as Coinbase and PayPal which facilitate the purchase and sale of cryptocurrencies. The majority of companies on this list are recognisable names with indirect, sometime marginal, links to cryptocurrency. The likes of Alphabet, Amazon and Mercedes-Benz Group do not derive a substantial portion of their revenue from Cryptocurrency.

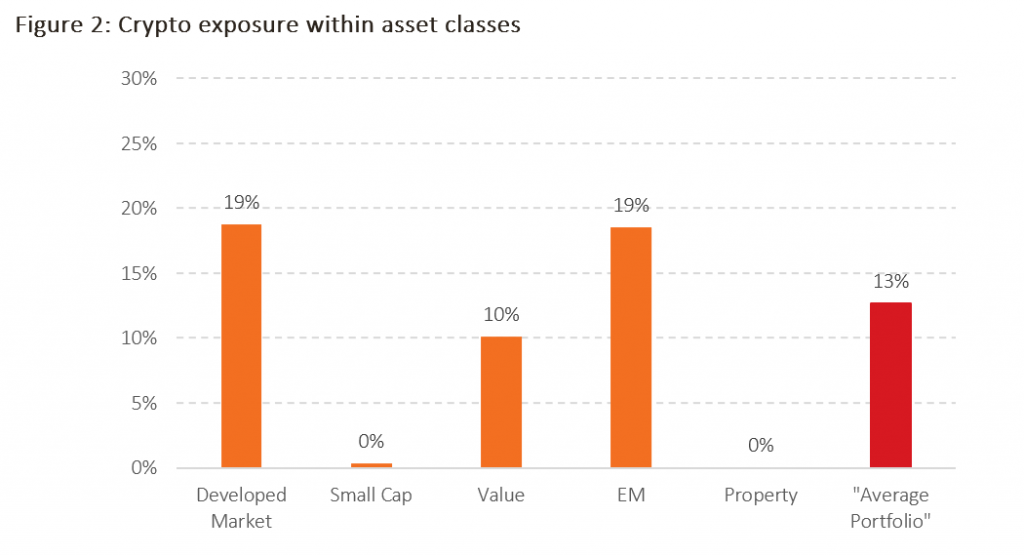

It is reasonable to expect some portion of globally diversified funds and portfolios to be invested in these stocks. The figure below provides an insight into the ‘crypto stocks’ exposure across various asset classes.

Source: Albion Strategic Consulting. Funds used referenced in endnotes

At first glance, having 19% of companies from the developed and emerging markets exposed to cryptocurrencies in some form, representing 13% of an average systematic portfolio (The “Average Portfolio” is based on the average Albion client community 100% equity portfolio and is a mix of 45.9% global developed equity, 15.3% global developed small cap, 15.3% global developed value, 13.5% emerging markets and 10% global commercial property) may be surprising. However, since the majority of funds held in client portfolios are systematic or index trackers, there is no active bet being placed on the sector. More importantly, this exposure can be seen as a benefit. Should cryptocurrencies, the blockchain industry or tokenization become mainstream technologies, this type of portfolio will be well positioned to benefit as they will own any future winners, which may be flying under the radar today. Moreover, considering many of the names in the list are large, recognisable firms whose primary purpose has nothing to do with cryptocurrency, these numbers become a lot less concerning.

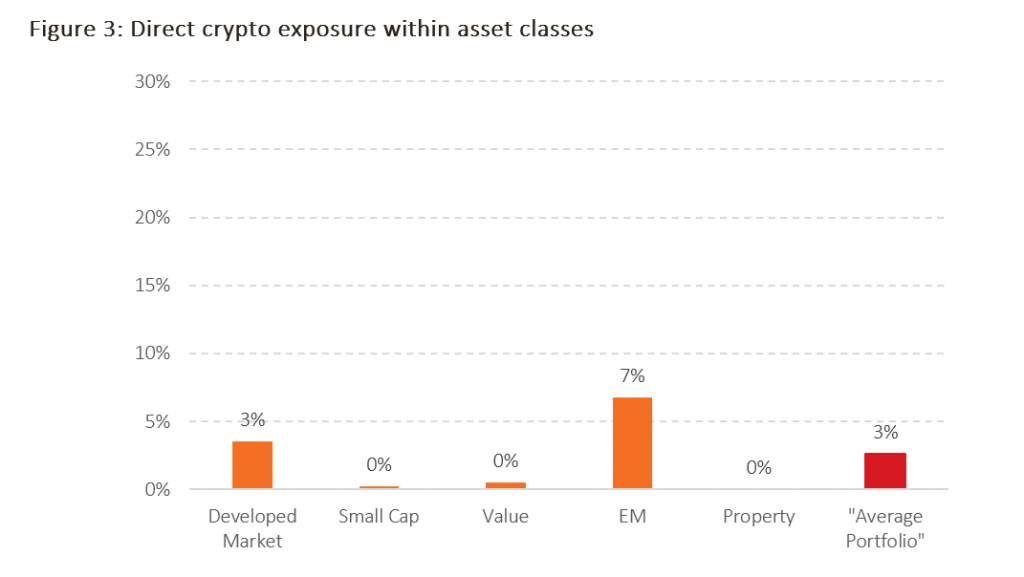

Taking a deeper dive, the exposure to ’direct crypto holdings’ (Direct exposure is taken from “Intended and Unintended Crypto Exposures” (March 2023, Morningstar Quantitative Research) and represents the top third of stocks in the list provided earlier in this note, ordered by net exposure to digital assets) are shown in the figure below. This demonstrates the reduction in crypto exposure when only considering those stocks that have the highest correlation to crypto markets. The numbers in the figure below mostly consist of two companies. Removing NVIDIA and Taiwan Semiconductor, two companies that since early 2023 have been more correlated with AI rather than crypto, reduces the numbers for developed market, emerging markets, and the ‘Average Portfolio‘ to 1%, 0% and 1% respectively. This demonstrates that although there is exposure to crypto in these funds, they are not overly exposed to the most volatile and high risk aspects of the cryptocurrency market.

Source: Albion Strategic Consulting. Funds used referenced in endnotes

Overall, the recent news in the cryptocurrency industry has not changed anything for the evidence based investor. The digital assets industry is large, and contributes to the world’s economy to the point they cannot be completely dismissed. Investing in systematic, diversified low-cost funds positions a sensible investor right where they would want to be. Diversified enough so that their portfolio is not overly impacted by moves in cryptocurrency markets, but still invested in companies that can provide the rewards of the innovation and advancements that blockchain technology might bring.

Risk warnings

This article is distributed for educational purposes and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy, or investment product. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.

Funds used for each asset class:

Developed market: Fidelity Index World

Small cap: Vanguard Global Small Cap Index Fund

Value: Dimensional Global Value Fund

EM: Vanguard Emerging Markets Stock Index Fund

Property: iShares Envir&LwCarb REIT